Traditional processes in conducting business in the digital world doesn't offer great transparencies and security. Because of the centralized design, it's controllable, but information and data manipulation are common.

This is where blockchain technology is gradually transforming peer-to-peer interactions in the modern digital world. Many large businesses are looking to this technology to improve the systems they are using.

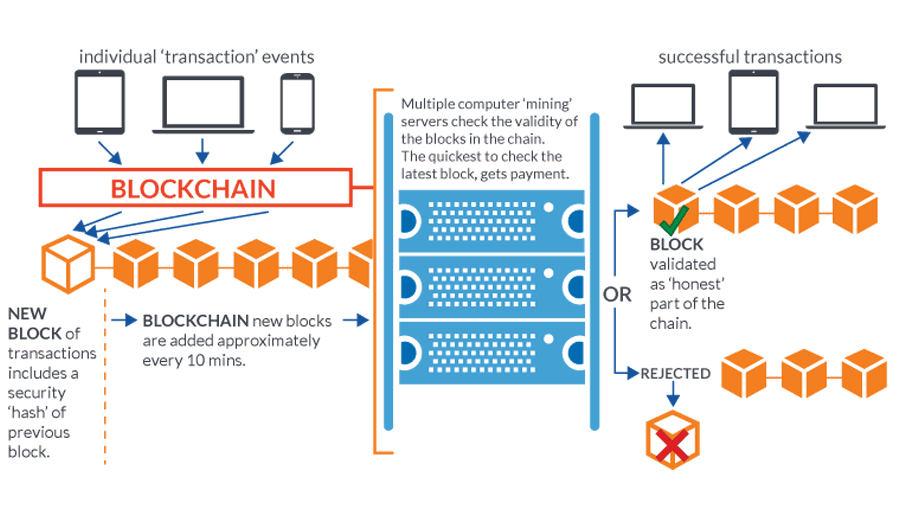

Consisting continuously growing list of records, called blocks, blockchains are linked and secured using cryptography. Each block typically contains a hash pointer as a link to a previous block, a timestamp and transaction data. Typically, it's managed by a peer-to-peer network collectively adhering to a protocol for validating new blocks.

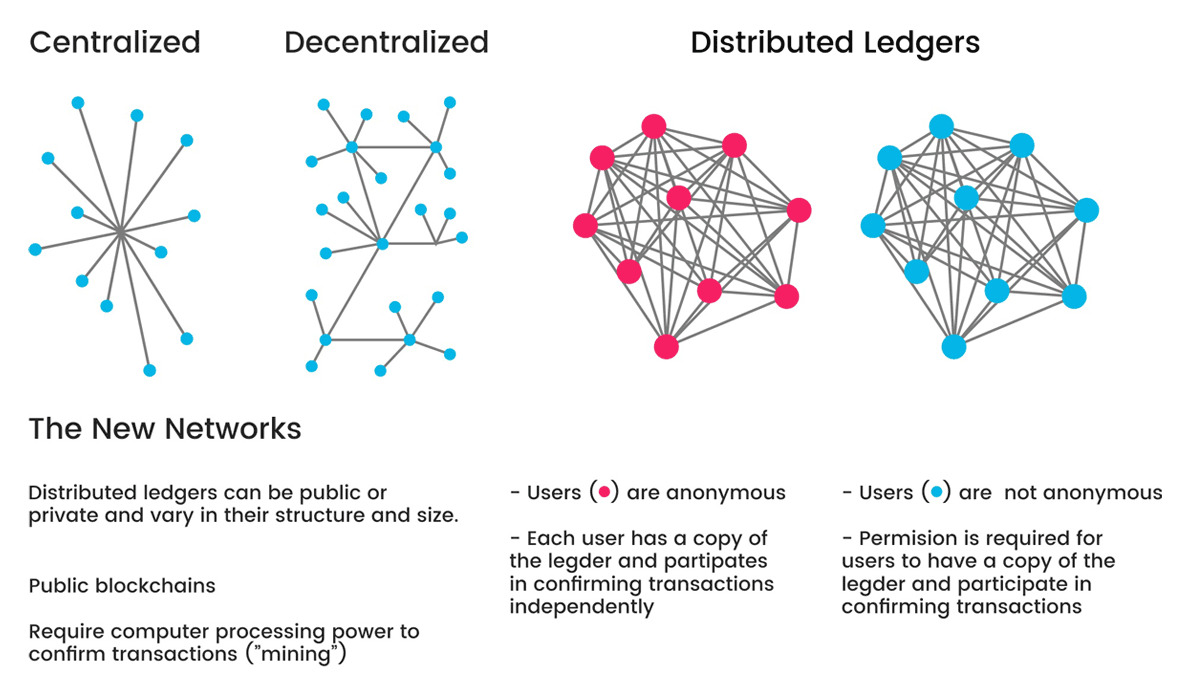

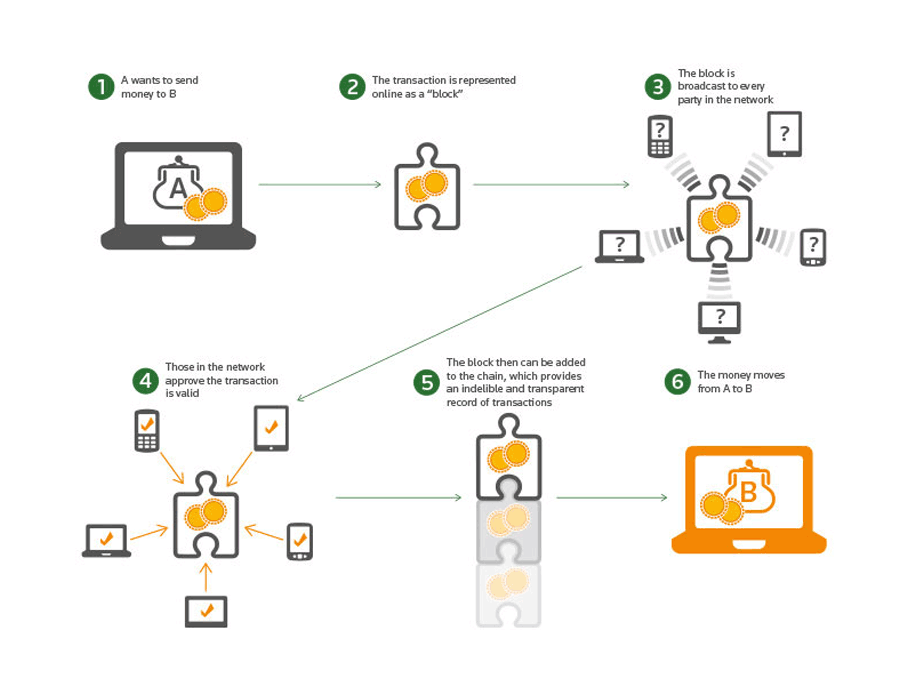

The technology facilitates secure online transactions by having distributed digital ledger that is used to record transactions across many computers. The open distributed ledger that records transactions between two parties efficiently and in a verifiable and permanent way.

So once recorded, the data in any given block cannot be changed without alteration of all subsequent blocks and the collusion of the network. The processes are authenticated by mass collaboration powered by collective self-interests.

The first distributed blockchain was conceptualized by Satoshi Nakamoto in 2008. In the following year, the technology was implemented as a core component of the digital currency Bitcoin. The invention of the blockchain for Bitcoin made Bitcoin the first digital currency to solve the double spending problem, without the use of a trusted authority or central server.

Blockchain's design has been an inspiration for others to apply similar decentralized design.

While providing transparency over an individual trade by making the accounting in any given transaction reviewable, the data is therefore public. What this means, all parties involved can access the blockchain, which updates itself after specified times.

For example, Bitcoin blockchain updates once every ten minutes.

Transparency and frequent updates eliminate data manipulation and common clerical issues found on manual and traditional processes.

Blockchain usually has its own Graphical User Interface (GUI) in the form of a wallet application. Those using blockchain, can use their wallets to purchase items and exchange cryptocurrency,

Read more: The History Of Bitcoin

Because of the advantages of blockchain, many businesses are trying to upgrade their current systems by adopting the technology. However, the technology has its own troubles. For example, the technology has barriers of entry, especially in the realm of smart contract technology.

A smart contract is computer code; a digital contract, a blockchain-based contract, or self-executing agreement that converts transaction deals into computer code. The data is then stored inside the system, and run by an international network of computers.

When Blockchain is running, the smart contract works as a self-operating program.

The result is the elimination of middlemen in the process of transaction, exchange of assets, physical or digital, or any contractual agreement which contains a set of verifiable parameters. In turn, if compared to traditional systems, blockchain is able to reduce transaction fees and lowering costs.

One example of a smart contract creator is the Etherparty. It's a application that is described as a contact wizard. The platform eliminates coding or programming by offering template libraries where users can create customized contracts.

The wizard will guide users through the process of creating the agreement and can choose from data sources or contract clauses. In addition, they can also test security, managing transaction fees, and use monitoring tools to manage their smart contracts throughout the whole process.

As a result, this eliminates the needs for people to go to lawyers to have contract papers notarized. With smart contracts, users can just drop their contractual agreement in the ledger.

In its simplest form, smart contracts are instructions added to transactions on the blockchain.

The advantages of blockchain is its security by design. Decentralized, the distributed computing system is potential for recording events, medical records, activity managements, transaction processing, documenting process, traceability and more.