Bitcoin and cryptocurrencies are trying to redefine how people see economy. But they have long struggled to find a safe haven on some popular online platforms.

One of which, is on Twitter. Its founder and CEO Jack Dorsey has publicly say that he is a 'fan' of Bitcoin creator Satoshi Nakamoto. Even his Twitter bio simply reads "#bitcoin".

However, Twitter itself is never a friendly place for any cryptocurrency.

This was again shown as an increasing number influential members of the Bitcoin and cryptocurrency community have complained that Twitter has "shadow-banned" them to limit their reach and impressions.

"They’re doing it, people," wrote Mike Dudas, the tech investor and founder of Bitcoin and cryptocurrency news and analysis website The Block, "Crypto Twitter has been shadow-banned. I’ve noticed this on my account this week."

Dudas was commenting on a previous complaint made by cryptocurrency developer Anthony Sassano who said that: "Any tweets that I post get way less impressions than normal."

Ryan Selkis, the CEO of Messari, a cryptocurrency news and rating site, said that they were having "ZERO impressions coming from accounts beyond TBI twitter followers."

"I think [Twitter] limited tweet reach [and] impressions," added the cryptocurrency policy think tank Neeraj Agrawal.

"I started using LinkedIn again out of desperation," further expressed Nic Carter, a partner at blockchain-focused venture capital fund, Castle Island Ventures.

At this time, Twitter has yet to respond to the comment.

But reports suggest that the platform's shadow-banning moves come as the Bitcoin community prepares for one of its biggest events: 'Bitcoin halving'.

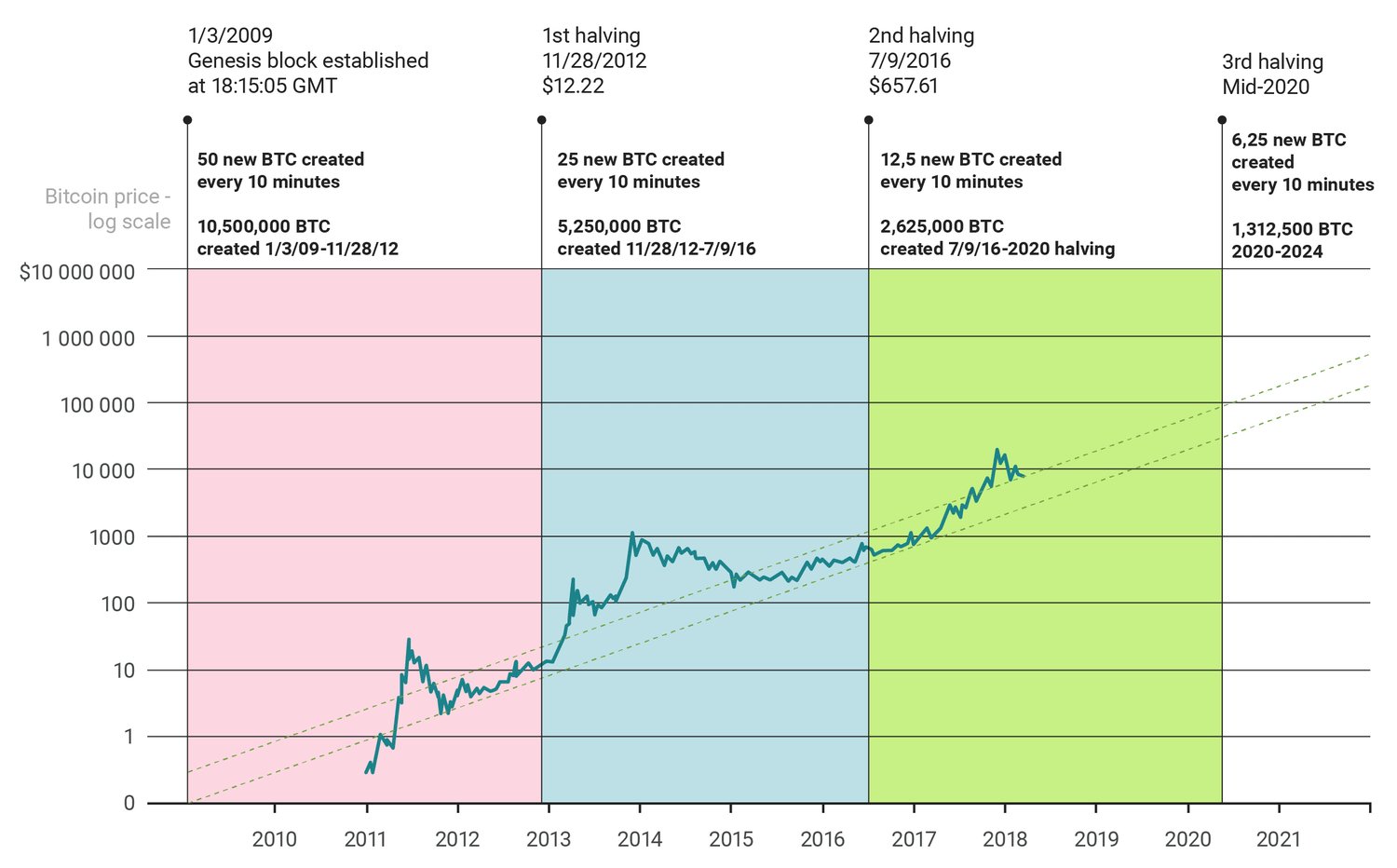

As a cryptocurrency needed to be 'mined', Bitcoin rewards those that maintain its network. For each block produced, a specific amount of Bitcoins are rewarded to the miners.

Initially when Bitcoin was first launched, miners could get 50 Bitcoins per block. On November 28th, 2012, the first Bitcoin halving occurred. Then in July 2016, the second halving took place

And in May 12, 2020, the third halving would take place, dropping the reward from 12.5 Bitcoin per block to 6.25.

While the amount of Bitcoin supply in the market can impact the price of Bitcoin, the halving is expected to rise its price. Experts expect Bitcoin trading volume to spike as the date closes to May 12, with a surge of media attention is expected to further push the cryptocurrency's price.

"After the two previous halvings, we've seen the price reach an all-time high within 3-9 months — which would be $20,000 in this case," one analyst said.

Danny Scott, co-founder and chief executive of CoinCorner, said that: "Coming up in 12 days is the bitcoin halving — which in short cuts the supply of bitcoins coming into circulation in half and taking it from 12.5 Bitcoins every 10 minutes to 6.25 Bitcoins every 10 minutes."

"People are looking at bitcoin's history and seeing how the supply and demand vector has played out for bitcoin in the past, with the price steadily rising after a halving to new all-time highs within 18 months," he added.

This can be seen in the first halving, which saw the cryptocurrency's price to increase from $11 to $1,000 around a year later. And in the second halving, the price of Bitcoin was trading at around $700, but a year later in 2017, the price skyrocketed to $20,000.

And Twitter here, sees a dramatic uptick in cryptocurrency scams across its platform, coming from fraudulent verified accounts to a general increase in copycat accounts.

In 2018, it was reported that Twitter touted its place in the cryptocurrency community, highlighting that notable individuals have tweeted about Bitcoin and other cryptocurrencies, while showing charts and data that indicated the size of the conversation was among the fastest-growing on the platform.

"We’re seeing Bitcoin ($BTC) conversation volume alone exceeding that of the FANG stocks (Facebook $FB, Apple $AAPL, Netflix $NFLX, Google $GOOG) on a daily basis," wrote the company at the time.

But Twitter however, appeared to be taking steps to defend its position.

Some Bitcoin traditionalists, like Bitcoin Core advocate Peter Todd, for example, when he reported that the Bitcoin Twitter account was misrepresenting Btcoin. Twitter's automated response to Todd was more like @bitcoin has violated the platform’s policies.

One Twitter user who experienced a temporary shadow ban once said that subjective moderation doesn’t help cryptocurrency communities.

“While I understand that’s frustrating, I also firmly believe that someone should be doing their own research on something and that they alone are responsible for the moves they make with their money,” once wrote @Joebwankanobee.

With Twitter yet to clarify how it finds and defines abusive behavior related to Bitcoin or cryptocurrency, many users will be left with the fear of losing their brand platforms by participating in Twitter game with unknown rules.