In the quiet corridors of Europe's established financial institutions, a profound shift is underway.

Just months ago, Belgium's largest bank-insurance group, KBC, flipped the switch on regulated Bitcoin and Ether trading for everyday retail clients through its familiar Bolero brokerage platform. What makes this move remarkable is not the assets themselves, but the seamless way they now sit alongside stocks, bonds, and mutual funds in a single, trusted client journey.

No new apps to download, no separate logins required: just another investment option in the banking environment customers already know and rely on.

This is not an isolated experiment. Across the continent, major players are reaching the same conclusion: digital assets belong inside the core banking stack, not parked on the sidelines.

For years, European banks approached crypto with understandable caution. Custody risks, compliance headaches, and a fragmented regulatory map made it easier to treat digital assets as a niche curiosity rather than a core offering.

Standalone platforms and third-party exchanges handled the heavy lifting while banks watched from afar.

That era is ending.

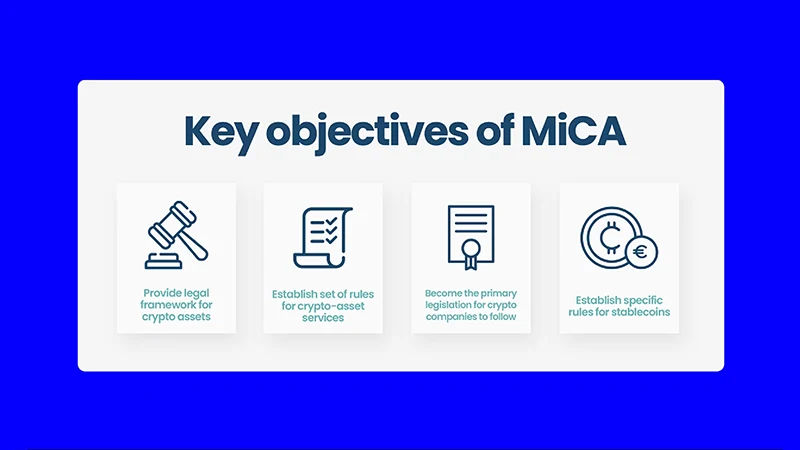

The catalyst has been the EU's Markets in Crypto-Assets Regulation, better known as MiCA, which replaced a confusing patchwork of national rules with a single, passportable framework. Suddenly, a bank in Madrid or Frankfurt could add crypto trading under the same operational and compliance standards it already applies to traditional securities.

The conversation changed from "Should we build something entirely new?" to "How quickly can we integrate this into what we already do exceptionally well?"

The evidence is mounting in real time. BBVA rolled out Bitcoin and Ether trading and custody directly to all its retail customers in Spain, making 24/7 access available straight through its mobile app.

Germany's DZ Bank, the powerhouse behind the country’s cooperative banking network, secured MiCA approval and launched its "meinKrypto" platform, letting clients of Volksbanken and Raiffeisenbanken trade major cryptocurrencies within their everyday banking apps. Société Générale, through its dedicated Forge subsidiary, has gone further still by issuing its own regulated euro and dollar stablecoins while tokenizing bonds and bridging traditional capital markets with blockchain rails. And now KBC joins the list, proving that even the most conservative institutions are moving at speed.

These are not fringe players; they are among Europe’s most heavily regulated and systemically important banks, and they are embedding crypto into the very infrastructure that powers millions of client relationships.

The implications stretch far beyond trading volumes.

When crypto arrives inside a regulated bank platform, trust travels with it. European banks already serve hundreds of millions of verified retail clients with established brokerage accounts and proven identities. A recent survey of thousands of investors across Germany, Italy, Spain, and France found that one in four already owns crypto, with adoption hitting 28 percent in Spain alone, and a striking 35% saying they would consider switching banks if a competitor offered better digital-asset services.

That pressure is real.

Banks that integrate now keep the customer relationship, the data, and the opportunity to cross-sell everything from tokenized bonds to structured products and wealth-management services built on digital rails. The old model, where crypto exchanges owned the client entirely, is quietly giving way to one where the bank remains at the center.

Even more transformative is the expansion into payments and settlements.

Bloomberg Intelligence projects that stablecoins could handle more than $50 trillion in annual payment flows by 2030, a figure that would reshape global finance.

European banks are not sitting idle.

A consortium including ING, UniCredit, BBVA, CaixaBank, and others is preparing Qivalis, a fully MiCA-compliant euro stablecoin slated for launch in the second half of 2026. Société Générale’s CoinVertible products are already live and being integrated into wallets and trading platforms. Tokenized deposits and on-chain settlement are moving from pilot to production, turning what once felt like science fiction into standard banking capability.

The competitive question is no longer banks versus blockchain. It is which banks will move fastest to capture this new layer of value.

This shows a fundamental reordering of market structure, where the future will not be defined by who lists the most tokens or racks up the highest exchange volumes. Instead, it will be decided by which institutions can deliver digital assets with the same effortless reliability they provide for every other financial product (trading, custody, payments, and beyond) at true production scale.

Some capabilities will be built internally; others will come through strategic acquisitions and partnerships, much as banks have historically absorbed market data providers or settlement systems.

The real power shift is distributional. Once crypto flows through the platforms that already reach the mass market, the addressable audience grows exponentially without a single new customer acquisition campaign.

Europe’s banks are no longer dipping a toe into crypto because they're now diving in with the full weight of their balance sheets, regulatory expertise, and customer trust.